According to the United Nations Office for Disaster Risk Reduction’s (UNDRR), 2025 Global Assessment Report on Disaster Risk Reduction (GAR):

“Earthquakes account for over a quarter (25.6%) of global economic disaster losses… Between 1970 and 2023, the economic cost of geophysical disasters like earthquakes accounted for an estimated USD 1.59 trillion.”

Their Multi-Hazard Event page states: “Between 2000 to 2023, five hazards triggered 90 percent of disaster deaths: earthquakes (50%), extreme heat (18%), storms (14%), floods (8%), and droughts (2%).”

Mitigation efforts lessen the impact of a disaster. Preparedness efforts help ensure a community is ready for whatever those impacts amount to. Less mitigation means a community must increase their preparedness efforts, because the impact from a disaster will be greater than it would have been if they’d mitigated.

For example, take a hardware store located in a floodplain. Nearby water ways are in need of dredging. The store has invested in wrapping their building with a low concrete parameter fence, save for the two driveways into the parking lot.

When news that a flood comes, they close the store and use in-house forklifts to move Jersey barriers into place at those driveways, fully enclosing the parameter. Then sandbags are added to help hold flood waters back, and store merchandise is raised 18 inches off the ground — above the deepest flood level the store has experienced — in case the flood breaches the barriers.

If dredging occurs prior to the flood (mitigation), the preparedness efforts done by the store (Jersey barriers and sandbags) are enough to prevent water from entering the store. Unfortunately, in this real example of a 2006 Tillamook, Oregon flood, the dredging had not been done.

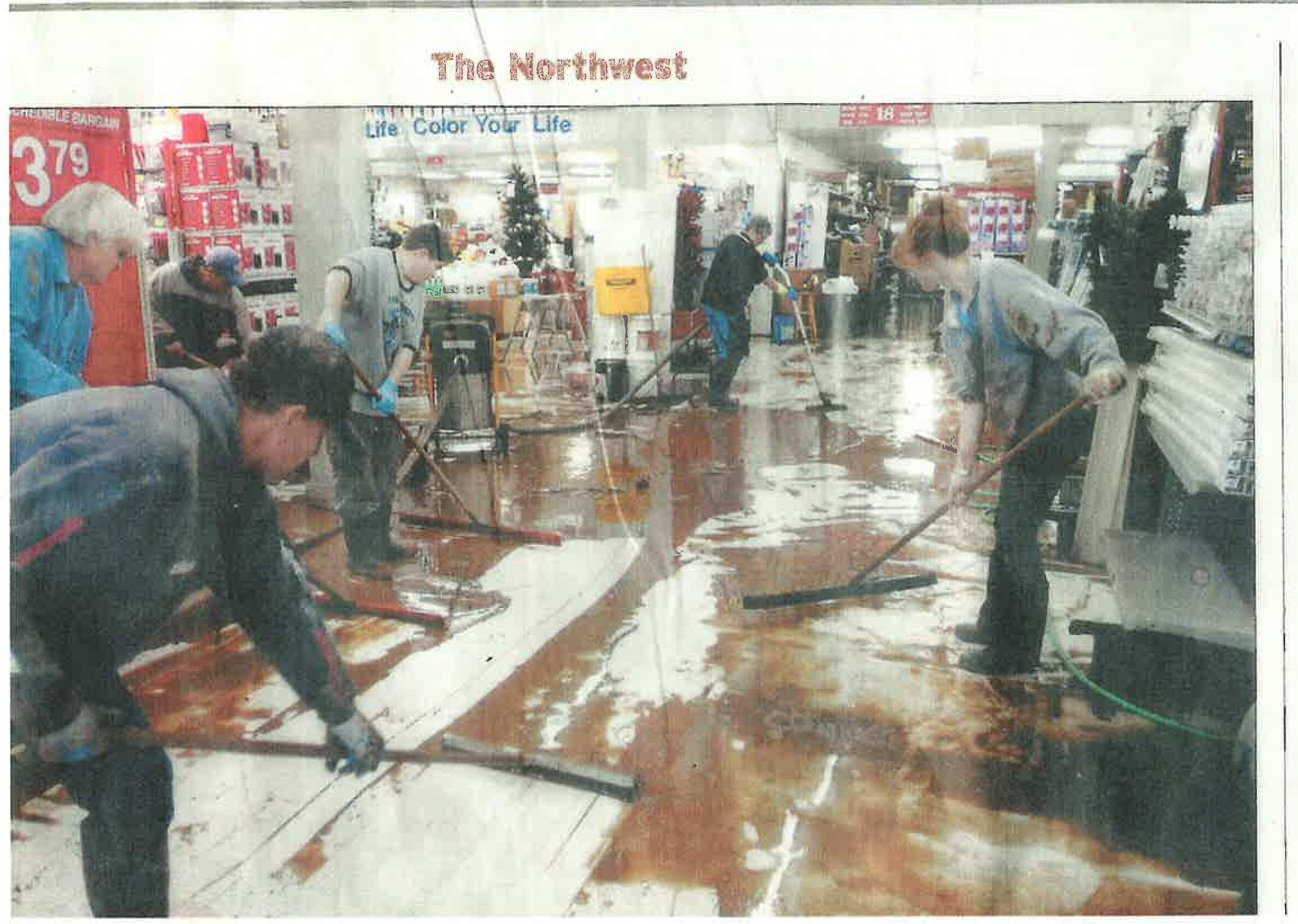

The Jersey barriers and sandbags worked well for several hours initially. I, along with about six other employees were in the store when the flooding reached the building. For hours, we were in a dry store watching the flood levels rise until eventually, waves were rolling inches above the bottom of our windows where Highway 101 should have been. If felt like being in a boat.

Without the dredging, the water level continued to rise until it eventually overcame the preparedness efforts. The store ended up with four feet of water in the first floor (thankfully there was a second story for us to be in). This is me on the right with my hair in a bun and rubber boots on, as I helped to squeegee the mess left behind. Mold grew on walls, employees and volunteers (my dad came to help. He’s the one on the left in the blue shirt) received Tentis shots to help protect against the bacteria exposure, and all the supplies below the flood level that had come in much above the “worst case” 18 inches, were thrown into garbage bins in the parking lot. The cost to the store was nearly a million dollars.

In the end, other preparedness efforts we had taken had still been helpful. We moved most people and their cars up and out of the flood zone before the water hit. We’d carried computers upstairs, so we didn’t lose the information. We saved what we could, but with mitigation, the efforts would have gone much farther.

The United Nations Office of Disaster Risk Reduction recently released the 2025 Global Assessment Report on Disaster Risk Reduction. Watch this short 2-minute video. When we discuss Cascadia, there is typically a C4 discussion: compounding, consecutive, concurrent and cascading events. Financing for preparedness, mitigation, response and recovery play a roll. Here are the three downward spirals discussed in the video below. The video gives brief explanations on how to break the spirals. Their main webpage (hyperlink above) provides detailed steps that households, nations, the private sector and the global community can take to break the spirals.

The decreasing income and increasing debt spiral: Disasters hit household incomes, shrinking tax revenue. Government borrows more. Debt becomes riskier. Interest rates go up. Disasters continue and funding recovery becomes increasingly difficult to impossible.

Unsustainable Risk Transfer Spiral: Disaster losses increase. Insurance gets more and more expensive, coverage drops. Premiums rise and sometimes insurers pull out.

Response / Repeat Spiral: Disasters hit. Aid flows in. Communities rebuild without addressing underlying vulnerabilities and the next disaster restarts the cycle, draining resources that could have funded prevention.